Cutting Benefits in Medicare: Truth or Fiction?

One of the flash points in the debate over healthcare reform legislation is whether the bills proposed in the House and the Senate would cut the benefits of Medicare beneficiaries. Of course, nothing can mobilize a group of senior citizens more quickly than a proposal to cut their benefits, and opponents of healthcare reform have claimed that the bills coming out of the House and Senate do just that. Are these claims valid?

The short answer is yes, at least for some beneficiaries who are enrolled in Medicare Advantage plans, which are private insurance company plans that receive Medicare dollars to deliver a package of benefits to replace Medicare Part A and Part B. One of the most signficant sources of savings in both the House and Senate bills is stems from changes in payments to Medicare Advantage plans.

Originally it was hoped that, by allowing private plans to participate in Medicare, beneficiaries might receive better coordinated care compared to fee-for-service Medicare and, if the private plans were more efficient than traditional Medicare, they might even save money for Medicare. For example, in a given region of the country, if Medicare beneficiaries on average consume medical services that cost the Medicare program $10,000 per year, there is the possibility that a private plan could deliver the same benefits for less than $10,000. If the Medicare program paid the plan $9,750 and the plan could deliver benefits for $9,500, the Medicare program would save $250 and the plan could make an extra profit of $250. To encourage plan participation, however, in recent years, for most areas (rates are actually set on a county-by-county basis), Congress has set the benchmark rates, which are the basis for payments to the Medicare Advantage plans well above the average per-beneficiary costs Medicare incurs in each area. The way the payment mechanism works is that plans bid against the benchmark rates for each county. If their bid is below the benchmark, they recieve their bid plus 75% of the difference between their bid and the benchmark, and the remaining 25% is retained by the Medicare program. So if the benchmark is $12,000 and the plan bids $11,000, the plan receives $11,750. According to the rules of Medicare Advantage, plans must use the extra $750 above the benchmark to provide extra benefits to beneficiaries. In this example, therefore, beneficiaries would receive an extra $750 in benefits. Compared to the regular fee-for-service Medicare program, however, the costs are much higher than the average per-beneficiary costs in each county. In this example, instead of incurring an average of $10,000 in costs, Medicare is paying the plan $11,750. And, while it is true that the beneficiaries in this case receive an extra $750 in benefits, Medicare is paying an extra $1,750 for those benefits. Because they can receive extra benefits, beneficiaries naturally like the Medicare Advantage program, and enrollment has soared in recent years. Now one in every four Medicare beneficiaries is enrolled in a Medicare Advantage plan.

The short answer is yes, at least for some beneficiaries who are enrolled in Medicare Advantage plans, which are private insurance company plans that receive Medicare dollars to deliver a package of benefits to replace Medicare Part A and Part B. One of the most signficant sources of savings in both the House and Senate bills is stems from changes in payments to Medicare Advantage plans.

Originally it was hoped that, by allowing private plans to participate in Medicare, beneficiaries might receive better coordinated care compared to fee-for-service Medicare and, if the private plans were more efficient than traditional Medicare, they might even save money for Medicare. For example, in a given region of the country, if Medicare beneficiaries on average consume medical services that cost the Medicare program $10,000 per year, there is the possibility that a private plan could deliver the same benefits for less than $10,000. If the Medicare program paid the plan $9,750 and the plan could deliver benefits for $9,500, the Medicare program would save $250 and the plan could make an extra profit of $250. To encourage plan participation, however, in recent years, for most areas (rates are actually set on a county-by-county basis), Congress has set the benchmark rates, which are the basis for payments to the Medicare Advantage plans well above the average per-beneficiary costs Medicare incurs in each area. The way the payment mechanism works is that plans bid against the benchmark rates for each county. If their bid is below the benchmark, they recieve their bid plus 75% of the difference between their bid and the benchmark, and the remaining 25% is retained by the Medicare program. So if the benchmark is $12,000 and the plan bids $11,000, the plan receives $11,750. According to the rules of Medicare Advantage, plans must use the extra $750 above the benchmark to provide extra benefits to beneficiaries. In this example, therefore, beneficiaries would receive an extra $750 in benefits. Compared to the regular fee-for-service Medicare program, however, the costs are much higher than the average per-beneficiary costs in each county. In this example, instead of incurring an average of $10,000 in costs, Medicare is paying the plan $11,750. And, while it is true that the beneficiaries in this case receive an extra $750 in benefits, Medicare is paying an extra $1,750 for those benefits. Because they can receive extra benefits, beneficiaries naturally like the Medicare Advantage program, and enrollment has soared in recent years. Now one in every four Medicare beneficiaries is enrolled in a Medicare Advantage plan.

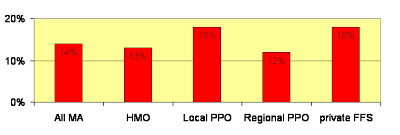

Medicare program payments relative to FFS spending, 2009

In 2009, in comparison with traditional fee-for-service Medicare costs, Medicare is paying Medicare Advantage plans an extra 14%. It is these extra costs that Congress has taregeted for savings. The House bill sets the benchmark rates at 100% of the average per-beneficiary fee-for-service Medicare costs for each county. The Senate bill sets the bechmark rates at the weighted-average bids of each plan. In either case, the savings would be substantial. With lower benchmarks, however, plans will not be in a position to maintain the level of extra benefits they currently provide, so these extra benefits would be cut. Therefore, it is true that these extra benefits would be cut, but the traditional benefits of Medicare Part A and Part B would not be cut.

posted by MSA Partners at

9:25 AM

![]()

0 Comments:

Post a Comment

Subscribe to Post Comments [Atom]

<< Home